DSCR vs Cash Flow

DSCR and cash flow are closely related, but they are not the same thing. Real estate investors often use both when analyzing a rental property, and understanding the difference can help you make better financing and acquisition decisions.

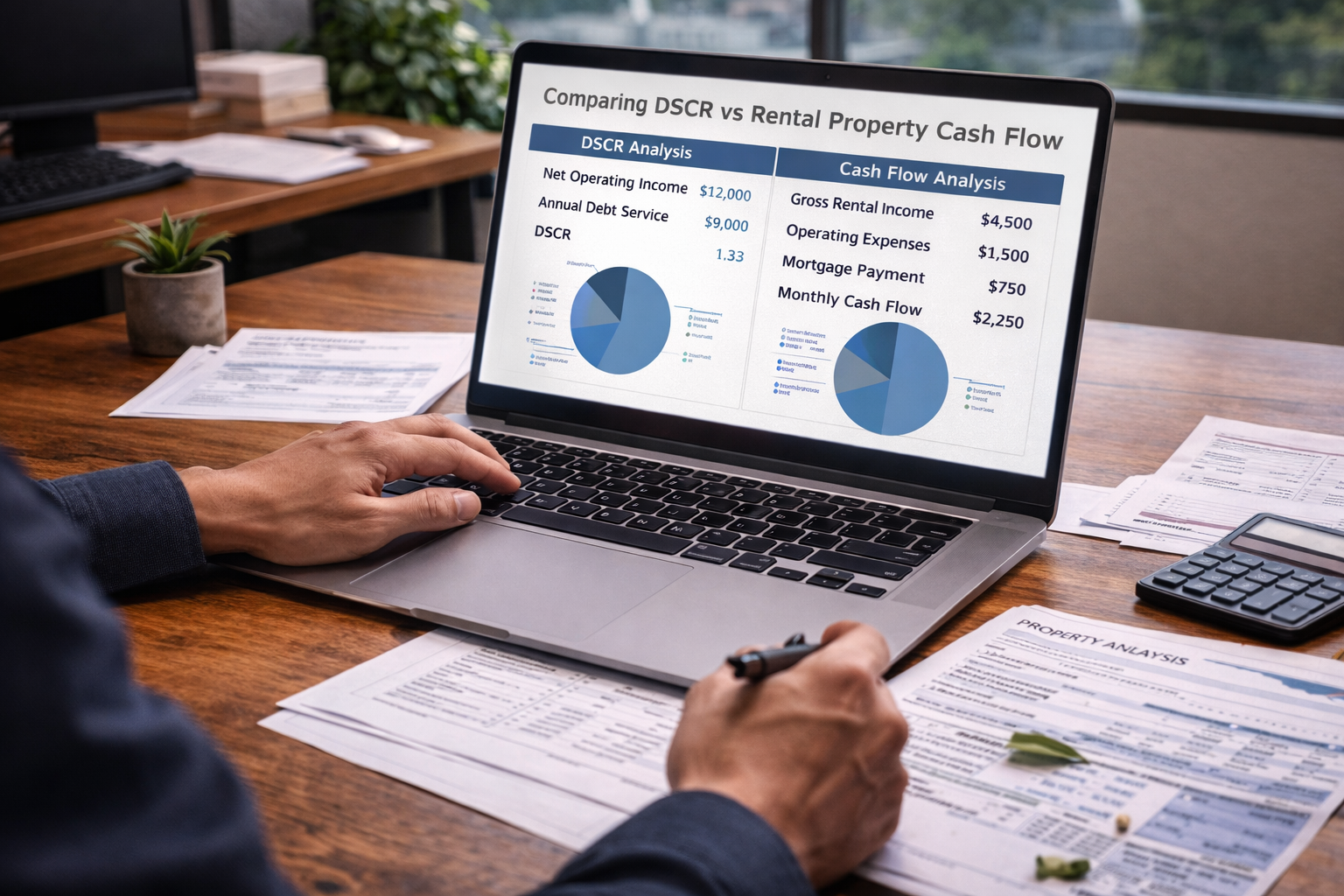

DSCR measures whether a property’s income covers its debt obligation. Cash flow measures how much money is actually left after the property’s expenses are paid. A rental can look strong on one metric and much weaker on the other, which is why serious investors should review both.

A property can qualify for DSCR financing and still be a mediocre investment. Strong debt coverage does not automatically mean strong real world profit after maintenance, vacancy, turnover, and management costs are considered.

What DSCR Means

DSCR stands for debt service coverage ratio. It measures whether a property’s income is enough to cover the monthly debt payment tied to the property.

The basic formula is:

DSCR = Rental income ÷ Monthly debt service

Monthly debt service usually includes principal, interest, property taxes, insurance, and HOA dues if applicable.

For a deeper breakdown of the metric itself, review What Is DSCR, How to Calculate DSCR, and What Is a Good DSCR Ratio.

What Cash Flow Means

Cash flow is the amount of money left after all income and expenses connected to the property are accounted for. It gives you a more complete picture of the property’s actual financial performance.

Cash flow usually considers:

- Rental income

- Mortgage payment

- Property taxes

- Insurance

- Property management

- Maintenance and repairs

- Vacancy allowance

- Capital expenditures

- HOA dues if applicable

- Other recurring operating costs

If you want a deeper property analysis framework, review How to Analyze a Rental Property Deal and How to Calculate Rental Cash Flow.

The Core Difference Between DSCR and Cash Flow

The main difference is that DSCR focuses on whether the income covers the property’s debt obligation, while cash flow focuses on how much money is actually left after the full expense picture is considered.

In simple terms:

- DSCR answers: Does this property support the loan?

- Cash flow answers: Does this property actually make money after real operating costs?

This is why DSCR is primarily a financing metric, while cash flow is primarily an investment performance metric.

Lenders care deeply about DSCR because they want to know whether the property can support the debt. Investors should care just as much about cash flow because that is what determines whether the deal is actually worth owning.

Example of DSCR vs Cash Flow

Suppose a rental property has the following monthly numbers:

- Rental income: $2,800

- Principal and interest: $1,850

- Property taxes: $250

- Insurance: $100

- HOA dues: $0

That gives total monthly debt service of $2,200.

DSCR = $2,800 ÷ $2,200 = 1.27

From a financing standpoint, that may look solid.

But now add:

- Maintenance reserve: $150

- Vacancy reserve: $140

- Property management: $224

- Capital expenditure reserve: $100

Now the remaining monthly cash flow is much lower than the DSCR alone might suggest. That is the gap investors need to understand. A property can show acceptable DSCR while still delivering thin real world cash flow.

Why DSCR Matters

DSCR matters because it is one of the main metrics used in investor lending. If the property does not generate enough income relative to the monthly debt obligation, financing options may be limited or pricing may be worse.

DSCR is especially important for:

- DSCR loan qualification

- Comparing financing scenarios

- Testing how interest rates affect loan feasibility

- Evaluating whether lower leverage improves the deal

- Screening acquisitions quickly

To go deeper, review DSCR Loans, DSCR Loans Explained, How DSCR Loans Work, and the DSCR Calculator.

Why Cash Flow Matters

Cash flow matters because it reflects the actual economic value of the deal to the investor. It helps answer whether the property produces enough profit to justify the risk, effort, and capital tied up in the investment.

Cash flow becomes especially important when:

- Evaluating true profitability

- Stress testing the deal

- Comparing self management versus professional management

- Planning reserves

- Measuring portfolio durability over time

Cash flow also helps investors avoid deals that technically qualify for financing but are too thin to be attractive in practice.

Can a Property Have Good DSCR but Weak Cash Flow?

Yes. This happens all the time.

A property may show acceptable DSCR because the lender is focused on rent versus debt service, but the investor may still face weak returns once management, turnover, maintenance, and future capital needs are considered.

This is especially common when:

- Maintenance risk is underestimated

- Insurance costs are rising

- Vacancy is ignored

- Management is treated as free

- Capital expenditure reserves are not included

That is why investors should not stop at DSCR alone.

Can a Property Have Weak DSCR but Decent Long Term Potential?

Sometimes yes, but it usually means the current financing structure or rent level is limiting the deal today.

A property may have weaker DSCR because:

- The interest rate is high

- The down payment is too low

- Current rents are below market

- The property is in transition or stabilization

- The investor is early in a BRRRR style repositioning plan

In these cases, the long term strategy might still work, but the current loan scenario may need to be revised.

For related strategy, review BRRRR Financing Guide, How Soon Can I Refinance, and Refinancing Investment Property.

DSCR Is a Loan Metric, Cash Flow Is an Owner Metric

One of the simplest ways to remember the difference is this:

- DSCR is how the lender views the property

- Cash flow is how the owner experiences the property

The lender wants to know if the debt is supported. The investor wants to know if the property is worth owning.

How Insurance and Operations Affect Cash Flow More Than DSCR

DSCR calculations usually include taxes and insurance within debt service, but they do not capture the full operational picture the way investors should. Rising insurance costs, tenant damage, maintenance surprises, and weak management can all erode cash flow even when DSCR still looks acceptable.

That is why investors often pair financing analysis with broader risk review such as Rental Property Insurance Cost, What Affects Landlord Insurance Cost, and Rental Property Risk Management.

How Investors Should Use Both Metrics Together

The best approach is to use DSCR first as a financing screen, then use cash flow analysis as the deeper investment filter.

A practical sequence looks like this:

- Check whether the property can support DSCR financing

- Review rent support and likely lender treatment

- Calculate realistic cash flow with reserves and management included

- Stress test the property for downside risk

- Decide whether the deal still makes sense after the full analysis

This helps prevent investors from overvaluing a property just because it qualifies for a loan.

When DSCR Matters More

DSCR tends to matter more when:

- You are trying to qualify for an investor loan

- You are comparing acquisition financing options

- You are evaluating refinance feasibility

- You want a quick first pass screening tool

When Cash Flow Matters More

Cash flow tends to matter more when:

- You are deciding whether a deal is actually worth owning

- You are measuring portfolio performance

- You are planning reserves and capital allocation

- You are stress testing long term hold quality

Missouri and Kansas Investors Should Watch Insurance and Property Condition Closely

In markets like Missouri and Kansas, DSCR may look fine at first glance, but insurance costs, wind and hail exposure, older housing stock, and deferred maintenance can weaken real cash flow faster than many investors expect.

That is one reason investors should include broader protection and operational analysis using resources like Portfolio Insurance for Multiple Rentals, Rental Property Disaster Insurance, and How Much Risk Can I Afford as a Landlord.

Related DSCR and Rental Property Guides

- DSCR Loans

- DSCR Loans Explained

- DSCR Calculator

- How to Calculate DSCR

- What Is a Good DSCR Ratio

- How to Analyze a Rental Property Deal

- How to Calculate Rental Cash Flow

- Rental Property Financing

If you want help reviewing whether a rental property works from both a DSCR and cash flow perspective, contact our team. We can help you evaluate financing structure, debt coverage, and the broader investment picture before you move forward.